At face value, it would seem that entering the crypto market after 2022 would be irrational. We’ve seen some of the biggest names in the business freeze their assets, close their doors and come crashing down like a meteorite. But where there is a crisis, there is also an opportunity.

Cryptocurrency, or crypto, is an innovative technology that has been around since 2009, the basis for which dates all the way back to at least 1983. It’s a decentralized form of currency that relies on a digital ledger (known as blockchain) to keep track of the transaction and ownership of each unit.

To call the crypto market a complex and convoluted system would be an understatement. There is so much going on under the hood that a whole book wouldn’t be sufficient to cover all the basics. Fortunately, you don’t need a Ph.D. to create a cryptocurrency token or app. In fact, even creating your own cryptocurrency is actually a very straightforward process. But should you? Seeking out professional software development services can help guide you through the complexities and determine if it’s the right move for your business.

Why Blockchain Technology & Cryptocurrencies?

With a fluctuating market, distrust toward crypto (anything Web 3.0 related), and a genuine preoccupation with the energy costs of blockchain, it would seem like this isn’t the best time to get involved. But, everything that’s going on is actually a very good thing. Hear me out.

The bad rep cryptocurrency is getting isn’t a byproduct of the technology itself, but rather the get-rich-quick culture that has surrounded it. Some readers might be too young to remember, but those of us who were there to see the rise of the world wide web remember the dot-com bubble and the crash that followed in the late 90s.

In short, thanks to the low-interest rates of the 1980s, we saw exponential growth in startups. Many of the new enterprises saw an opportunity in a disruptive technology called the internet. This translated to a massive surge in e-commerce, and for many companies, this was their catapult toward success (Amazon for example). Many others died out, unable to become profitable in a market that was beyond saturated.

On top of it all, we saw everything from impossible promises (at least at the time) to scams and ill-defined projects. Sound familiar? New technologies bring both dreamers and opportunists who rely on the potential of the tech to sell a possibility, a dream, a mirage.

But such lofty promises are unsustainable in the long term, and the inevitable crash ends up separating the wheat from the chaff. The dot-com craze gave us PayPal, Google, Amazon, and dozens of companies that grew way beyond their initial idea.

Cryptocurrency is going through its painful adolescence, and that’s a good thing, as these shake-ups are necessary for a market to mature and grow. There are plenty of reasons to be carefully optimistic about the future to come.

How to Make Your Own Blockchain & Create a Cryptocurrency The Easy Way

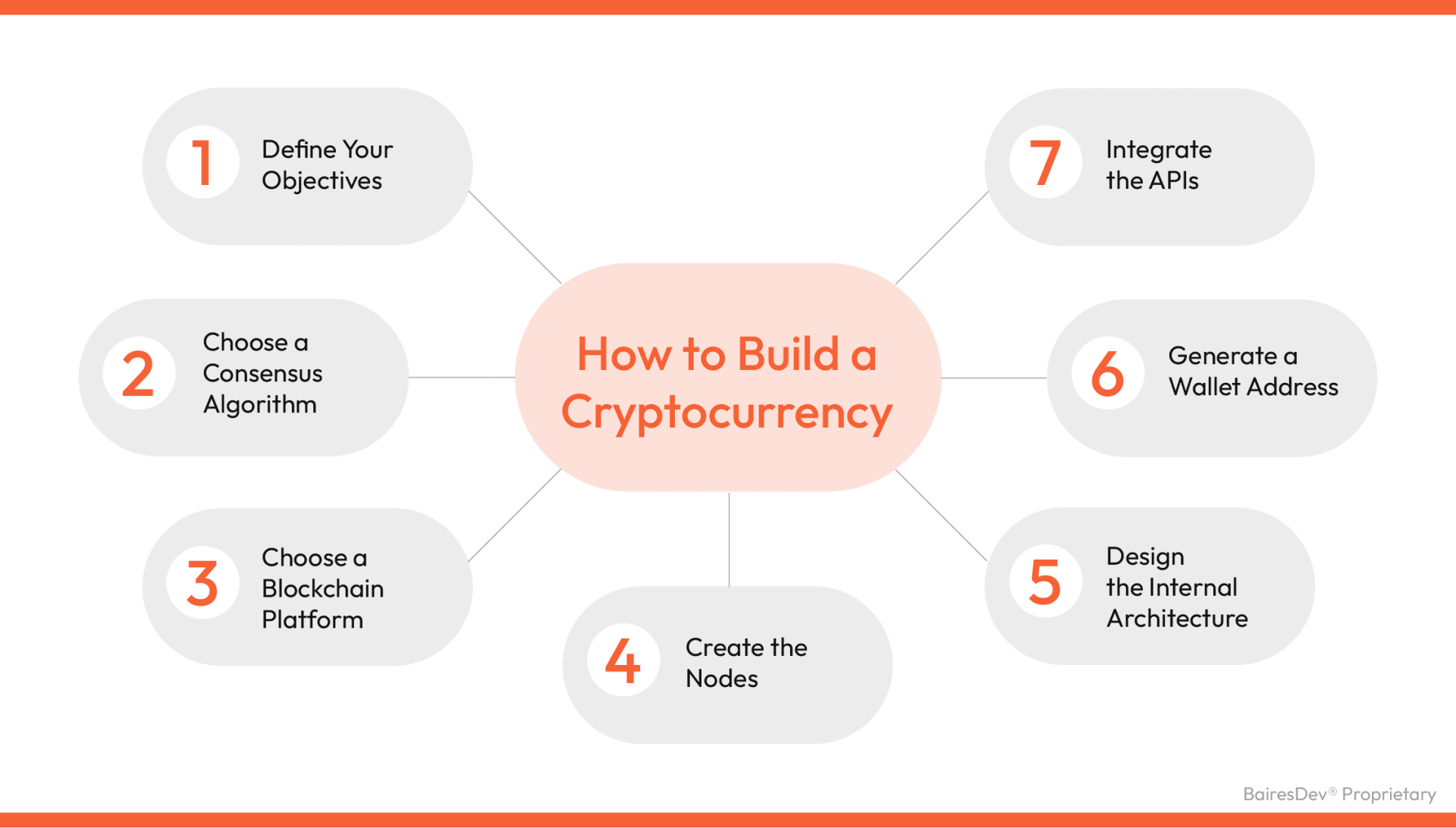

There are many approaches one could take to build a cryptocurrency. The history of Bitcoin is evidence of just how convoluted and complex it can be. Fortunately, thanks to the growing popularity of the technology, the process has been streamlined to the point where you can summarize it in seven steps:

#1 Define Your Objectives.

The first step is determining why you want to create a cryptocurrency. Not everyone who starts a project like this is trying to topple Ethereum and Bitcoin as the reigning champions. Sometimes you want something small; for example, cryptos are great for building brand awareness, raising capital, or as a foundation for a rewards program.

Your objective will help you understand the scale of the project and choose the best approach in each of the following steps.

#2 Choose a Consensus Algorithm

Decentralization is a core tenet of cryptocurrencies. To maintain this decentralized structure, cryptocurrencies rely on consensus mechanisms to verify transactions on the blockchain.

Understanding the intricacies of this mechanism is pivotal in comprehending how cryptocurrencies operate on a secure and transparent blockchain architecture.

The two most prevalent consensus mechanisms are proof of work (PoW) and proof of stake (PoS). Each of these methods plays a pivotal role in ensuring the validity and security of cryptocurrency transactions:

Proof of Work (PoW): In the PoW consensus mechanism, multiple participants, often referred to as miners, engage in a competitive race to validate a transaction. They achieve this by performing complex cryptographic calculations. The first miner to successfully complete these calculations is rewarded with a token or coin for their diligent effort. PoW is renowned for its robust security features, making it a reliable choice for many cryptocurrency networks.

Proof of Stake (PoS): In contrast, the PoS consensus mechanism takes a different approach. Here, participants, known as validators, are required to commit a certain amount of cryptocurrency resources as a stake. The higher the value of the stake, the greater the likelihood of a validator being chosen to confirm transactions and add new blocks to the blockchain. However, if a validator behaves dishonestly or makes errors, they risk losing their stake. PoS is lauded for its eco-friendliness, as it consumes significantly less energy compared to PoW.

The choice between these two consensus mechanisms is a crucial decision for anyone involved in cryptocurrency creation. While PoW is known for its robust security, PoS offers a greener and more sustainable approach. However, there is no universally correct answer when it comes to selecting the most suitable consensus mechanism. The decision should align with your cryptocurrency’s objectives and the goals you aim to achieve within the blockchain architecture.

#3 Choose a Blockchain Platform.

Yes, you could build your own blockchain from the ground up. But there are easier ways to create your own cryptocurrency. You could either grab the source code of an open-source blockchain platform and use it as a basis for your own blockchain, or you can use already existing blockchains.

Which blockchain to choose depends on your decision in the last step. Cardano and Polkadot are well-known proof of stake solutions. Ethereum, probably the most popular blockchain on the planet, is proof of work, but they are migrating their operations toward proof of stake.

#4 Create the Nodes

Nodes are the computers that participate in the blockchain network. They run the software protocol, validate transactions and keep the network secure.

You have to make a few choices at this step: Will the nodes be public or private? Will you have them on site or in the cloud? How many nodes? Which operating system are they going to run?

#5 Design the Internal Architecture

Now you have to build the internal architecture. This step is extremely important since once you go online there is no turning back. Aside from the technical aspect, you must make some important decisions regarding accessibility and the economy of your currency:

- Define who can access, create, and validate new blocks;

- Create the rules for asset issuance;

- Build a management system for private key protection and storage;

- Decide on the number of digital signatures your blockchain will require to verify the transactions;

- Estimate the block reward, block size, transaction limits, etc.;

- Estimate how many coins you’ll offer.

#6 Generate a Wallet Address

Now that your nodes are up, you need to have an address so people can interact with your network to buy or sell cryptocurrency; that’s your wallet address. You can generate it on your own or use a third party to create the address for you.

#7 Integrate the APIs

While this step is optional, it’s a good idea to think about an API for your cryptocurrency, as this will allow your users to build new tools and interact with your network in inventive ways. APIs are a fantastic way to build trust with a community of developers and tech enthusiasts.

Is It Legal to Create Your Own Cryptocurrency?

The short answer is yes. The long answer: it’s complicated.

Cryptocurrencies are in a gray area right now. Some countries accept them wholeheartedly, others only accept a few, and some ban them altogether. Depending on what you want to use your cryptocurrency for and your potential market, you might have to get acquainted with the legality of crypto.

Aside from that, some companies offer a seal of approval for cryptocurrencies, a great asset for any company that’s trying to make a break in the world of crypto. As long as you follow these steps and understand the laws regulating your market, there is nothing to fear.

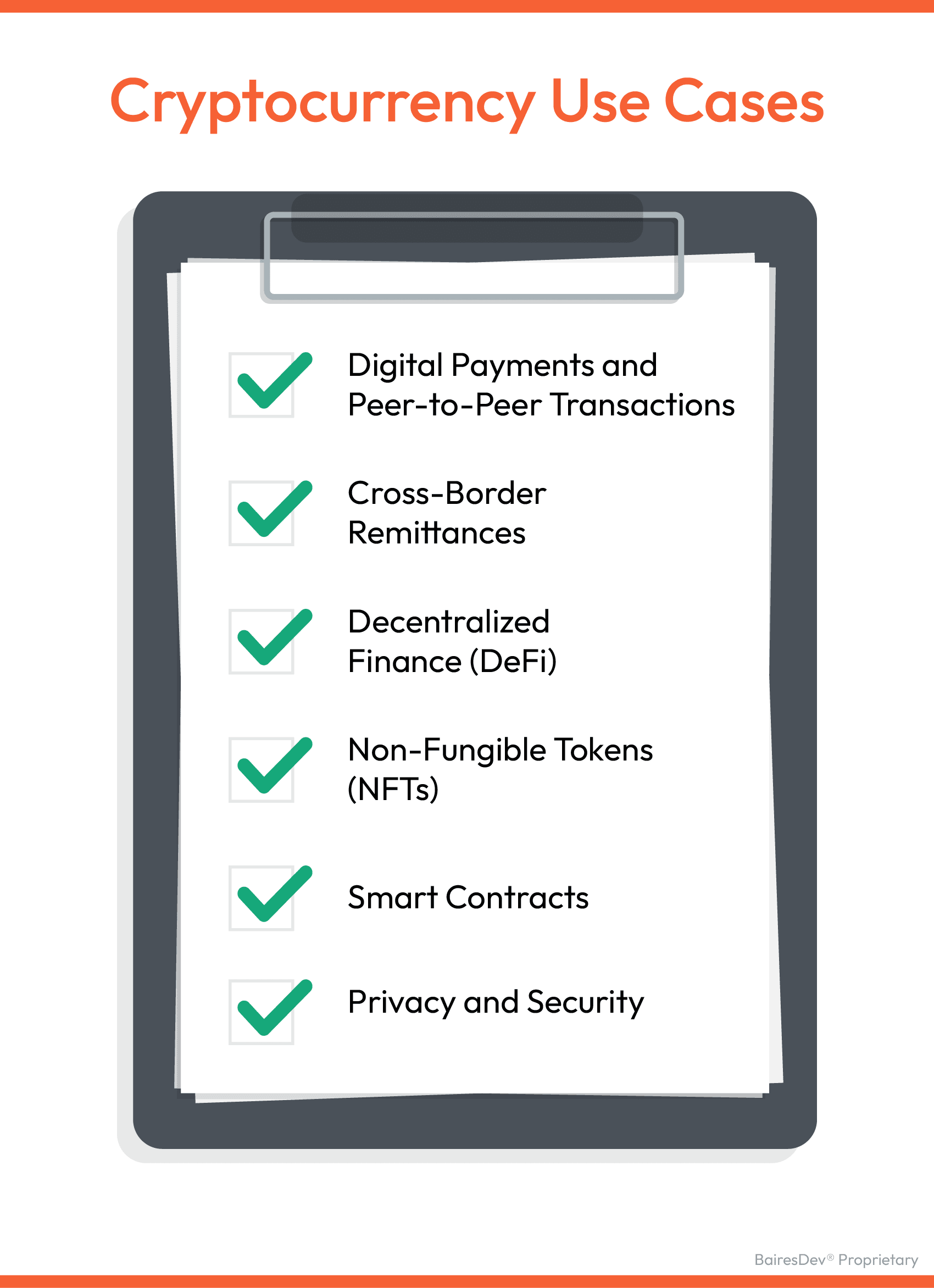

Cryptocurrency Use Cases

Cryptocurrencies have evolved beyond just being a digital alternative to traditional currencies. They serve a range of practical purposes, each with unique benefits and applications. Understanding these use cases is crucial for anyone considering creating their own cryptocurrency. Let’s explore some of the most prominent ones:

#1 Digital Payments and Peer-to-Peer Transactions

Cryptocurrencies were originally created to enable secure and decentralized peer-to-peer transactions without the need for intermediaries like banks. Bitcoin, the first cryptocurrency, paved the way for digital payments. Users can send funds across borders quickly and with lower transaction fees compared to traditional banking systems.

Real-World Example: Bitcoin (BTC) remains the most widely used cryptocurrency for everyday transactions. Many businesses, both online and offline, accept Bitcoin as a payment method. For instance, Overstock.com and Shopify allow customers to pay with Bitcoin for a variety of products.

#2 Cross-Border Remittances

Cryptocurrencies offer a cost-effective solution for international remittances. People working abroad can send money back home to their families without the high fees associated with traditional remittance services. This use case is particularly valuable for individuals in regions with limited access to banking services.

Real-World Example: Ripple’s XRP is often used for cross-border remittances. Companies like MoneyGram and Western Union have explored partnerships with Ripple to leverage its blockchain technology for faster and cheaper international money transfers.

#3 Decentralized Finance (DeFi)

DeFi is a booming sector within the cryptocurrency space, offering financial services without relying on traditional banks. DeFi platforms allow users to borrow, lend, trade, and earn interest on their cryptocurrencies. This ecosystem is known for its openness and accessibility.

Real-World Example: Compound Finance and Aave are popular DeFi platforms that enable users to earn interest by lending their cryptocurrencies or borrow assets by using their crypto holdings as collateral.

#4 Non-Fungible Tokens (NFTs)

NFTs represent ownership of unique digital assets and have gained immense popularity in the worlds of art, gaming, and entertainment. They are often used to prove ownership and authenticity of digital or physical items, including artwork, music, collectibles, and in-game assets.

Real-World Example: The sale of digital artwork as NFTs has taken the art world by storm. Artists like Beeple have sold NFT-based artworks for millions of dollars on platforms like OpenSea and Rarible.

#5 Smart Contracts

Smart contracts are self-executing contracts with the terms of the agreement directly written into code. They automate processes and eliminate the need for intermediaries in various industries, including legal, insurance, and supply chain management.

Real-World Example: Ethereum is the leading platform for creating and executing smart contracts. Companies like Chainlink provide oracles that enable smart contracts to interact with real-world data, expanding their functionality.

#6 Privacy and Security

Cryptocurrencies provide an added layer of privacy and security for users who want to keep their financial transactions confidential. Privacy-focused cryptocurrencies offer enhanced anonymity features.

Real-World Example: Monero (XMR) is a privacy-focused cryptocurrency that uses advanced cryptographic techniques to obfuscate transaction details, ensuring user privacy.

When creating a cryptocurrency, it’s crucial to comprehend the different use cases in the market, including payments, decentralized finance (DeFi), NFTs, and more, to make informed decisions. Consider tailoring your cryptocurrency’s features and capabilities to cater to a specific purpose. This approach allows you to leverage the existing blockchain infrastructure effectively.

The possibilities in the ever-evolving crypto space are wide open. By aligning your project with a particular use case, such as DeFi or NFTs, you can innovate within that area and potentially drive more adoption. However, it’s essential to navigate the legal aspects of cryptocurrency creation, ensuring your cryptocurrency complies with the relevant regulations.

As a blockchain developer embarking on the journey to create your own cryptocurrency, understanding the intricacies of cryptocurrency legal requirements is paramount. You’ll need to stay informed about the latest developments and identify opportunities to provide real utility within the crypto coin you’re developing.

With so many directions to explore, an insightful approach, combined with a deep understanding of existing blockchain infrastructure, cryptocurrency coin creation, and legal considerations, will serve you best when designing a new cryptocurrency.

How To Make a Cryptocurrency: Summing It Up

If you enjoyed this article, be sure to check out our other articles about Blockchain Technology:

- Blockchain Can Be a Strategic Ally for Healthcare. Here’s Why.

- Blockchain in Banking: A Game Changer for Financial Services

- How IoT, AI and Blockchain Lead the Way Towards a Smarter Energy Sector

- Is Blockchain a Solution Waiting for a Problem To Solve?

- What is Blockchain and Why Does Your Business Need it?

FAQs

Can creating a cryptocurrency be profitable in the long run?

Creating your own token can be profitable in the long run, but it is a risk. The success of creating cryptocurrency depends on a number of factors, including market demand, the technology you use, and more. Before you decide to build cryptocurrency, you should evaluate the risks vs. rewards.

What are some of the advantages and disadvantages of using an existing blockchain platform to create cryptocurrency?

There are several advantages of using an existing blockchain platform to create a new cryptocurrency, such as stronger security, community, cost savings, and seamless integrations with related applications. However, there are also some disadvantages, including limited customization options, greater competition, reliance on the platform’s infrastructure and development team, and governance that can affect your decision-making abilities.

What are the risks associated with creating a cryptocurrency, and how can they be mitigated?

There are some risks associated with creating your own crypto coin. For example, there are regulatory risks. Organizations can address this by working with legal experts to ensure cryptocurrency compliance. Additionally, cryptocurrency can be vulnerable to cyberattacks. That’s why it’s important to work with cybersecurity experts to rigorously test and assess the product first.

What technical skills are required to create a cryptocurrency?

Creating a cryptocurrency typically requires knowledge in blockchain technology, cryptography, smart contracts, and programming languages like Solidity for Ethereum-based tokens or C++ for custom blockchain solutions.